Even as the outbreak of Coronavirus (Covid-19) has spread from the Asian region to Europe and the US, it has endangered the expectations of a global recovery in 2020.It has emerged as the biggest global concern, crippling major economies and increasing the risk of a global recession. Covid-19 is expected to weaken the domestic growth impulses too by acting through the trade and financial channels. These are clearly uncertain times, one which require expeditious policy redressal measures-both on fiscal and monetary front. Consequently, CII suggests the following measures to ward off much of the adverse consequences on growth due to outbreak of Covid-19:

Fiscal Policy

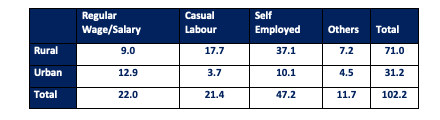

1. Need a serious fiscal stimulus of around 1 per cent of GDP amounting to Rs 2 lakh crores. This should be in the form of money in the hands of people through Aadhar based Direct Benefit Transfer. With oil prices coming down and the government raising excise duty, the government is expected to gain revenues to the tune of Rs 39,000 crore1. Every $10 dollar decline in the oil price leads to a saving of $15 billion in the oil import bill. Rs 5,000 can be transferred to the people with income less than Rs 5/10 lakhs. This can be for all persons greater than 18 years of age. For more vulnerable persons above 60, it can be raised to Rs 10,000. Since the income data is not available, we cannot calculate the number of people who will be eligible for the cash transfer. However, with a budget constraint of Rs 2 lakh crore, we can say that 20 crore people can be compensated with a transfer of Rs 10,000 each. The data on workers in different categories is given below and shows that there are roughly 20 crore casual labourers who are employed. They can certainly be compensated from the government’s fiscal resources.

Number of workers (15+ years) in different categories (in crore)

1. To make additional tax-related announcements:

a. Long-term capital gains tax of 10% to go

b. Tax on dividends at 25%

2. Government to pay their dues to the private sector, whatever the additional cost.

Monetary Policy

1. Reduction in interest rate – minimum 50 basis points

2. CRR reduction by 50 basis points

3. RBI to change definition of NPA recognition from 90 days to 180 days till September 30. Similarly, SMA guidelines to be relaxed till September 30: SMA-1 from 60 to 90 days and SMA-2 from 90 to 180 days and beyond that can be considered NPA.

Impact of COVID-19 on MSME Sector and CII Recommendations

The present coronavirus outbreak is a serious pandemic of unforeseen proportions. As of now, there is no end in sight despite strong efforts being made by the Governments across the globe.

Impact on sectors

Import-dependent sectors such as auto components (where SMEs have a share of 25-30 per cent in the value chain) and pharma bulk drugs (where the SME share is 35-40 per cent in the value chain) can withstand headwinds in the near term, given their inventory of one to two months. However, as inventories run down, the pressure will increase.

In export-dependent sectors such as apparel (SME share 25-30 per cent in the value chain), leather (SME share 80-85 per cent in the value chain) and ceramic tiles (SME share 50-55 per cent in the value chain), exporters are hopeful of an increase in orders, including from new geographies, because of manufacturing disruptions in China. However, the benefits are likely to be limited, amidst expected moderation in global GDP growth.

Meanwhile, commodity prices such as steel will come under pressure as demand declines. This will impact refractories, steel re-rollers, and the pig iron industry, which have a sizeable MSME presence.

Major challenges

Some of the major challenges faced by MSMEs would be with labour force and bank loans, as there would be expenses on paying salary and EMIs.

Cash Flows: Considering that the activity slowdown in commercial establishments can vary from 15 to 30 days, losses on account of fixed expenditure and severe disruption of cash flows would be seen. The MSME sector will have a tough time to address the loss and cash flow issues, during the period. The possible losses in case of such contingency are wages, minimum electricity bill and payments of bank dues.

Wage bills & payments: For wages, the legal interpretation of such a temporary shutdown is that it will be considered as Temporary Retrenchment and the employer is liable to pay 50% of the wages which the industry especially the MSME is not in a position to pay.

Inventory Management: MSMEs are overly reliant on a single geography or a single supplier for key products. They do not have enough visibility across the extended supply network to foresee their risks. Many lack integrated systems to understand their inventory status, to project stock-outs of direct materials and optimize production, or to project stock-outs of finished goods to optimize customer allocation, further lacking flexible logistics networks to ensure the flow of goods in a profitable manner. Items with low shelf life will face problems, both in case of raw material and finished products.

Inventory will be second biggest load over the MSMEs after wage bill. Carrying inventory for a longer time without adequate demand will heavily impact the business cycle.

Nonetheless, many MSMEs procure raw materials against specific order only. Therefore, such MSMEs shall face problems only if their buyers cancel the order or default on the contracts.

Time in Bouncing Back: We should keep in mind that tendency of MSME to bounce back will also depend on the sector it represents. Assuming the slowdown is for 2 months, the services sector still will have the ability to bounce back in a month or two but the manufacturing sector will take 6 – 12 months to come back, that too if the MSME has been a sustainable or profitable unit.

Recommendations

In the view of the above, CII suggests creation of a corpus by Government of India for supporting MSMEs to tide over the crisis.

Indian Industry would need to activate a three-pronged strategy:

1. Import side – Minimize risks to key sectors arising from supply chain disruptions

2. Export side – Leverage opportunities to be an alternative destination

3. Domestic manufacturing – Keep the supply chains running and leverage excess capacity

To overcome the Cash Flow and Working Capital challenges following are suggested:

- Deferment of all term liabilities by banks without levy of penal interest for minimum 6 months

- Routine defaults / delay in retiring LCs, if any, may be allowed with an extension of 3-7 days by banks.

- NPA norms in genuine cases may be extended to 180 days from present 90 days.

- Ad-hoc limits to an extent of 25% of sanctioned limits may be allowed by banks on SOS basis if required by industry to overcome temporary liquidity crunch.

- Delays in discharging social security liabilities may be condoned without any penal action for next 6 months.

- Larger companies, PSUs and Government departments may be instructed to release payment of MSME vendors out of turn against some reasonable discount if required by the said vendor so as to overcome his/her liquidity issues.

- GST Council may allow deferment of GST deposit by MSMEs with minimum one-month lag.

Impact of COVID-19 on Aviation Sector

The Indian aviation sector has been severely hit by the coronavirus outbreak. In the last one month, over 600 international flights to and from India have been cancelled for varying periods. Close to 500 of these were by foreign carriers and the rest by Indian operators flying overseas. The number of international passengers arriving at the country’s airports has come down to around 62,000 per day from 70,000 in the wake of the coronavirus outbreak. Considering the new visa restrictions, this number is likely to dip further.

Domestic travellers are also not moving, drop is primarily for flights to major metro cities like Delhi, Mumbai, Hyderabad, Bangalore, which are the prime revenue generators on the domestic front. The Indian aviation sector is looking towards Government of India with a great hope and seeking for contingency funds and temporary bailout packages to financially support the aviation sector.

Challenges:

- Cash reserves are running down quickly as fleets are grounded and operating flights are less than half full

- Over the past few days, on a week-on-week basis, companies have seen a 15-20 per cent decline in daily bookings.

- India is also witnessing a drop up to 30 per cent in international visitors, International air travel to and from India has already been hit due to travel ban and warning issued by many countries, including those from West Asia. This has led to tourism industry being almost shut down

- Domestic travellers are not moving, drop is primarily for flights to major metro cities like Delhi, Mumbai, Hyderabad, Bangalore, which are the prime revenue generators on the domestic front

- Expecting flight and freight reduction by over 60 per cent in the coming months

- The Ground Handling industry is a labour- and capital-intensive sector. The industry employs over 70 thousand people with their associated families being dependent. Any adverse effect of the scale, as is expected today, could necessitate serious cost cutting measures by the industry to stay afloat. It may even take some to the brink of closure.

- Huge amount of Payroll Obligations to pay like: Airport receivables, Rentals, Statutory obligations etc.

Recommendations:

It is important to look at avenues to reduce overall operating costs, therefore:

- Parking and landing fees should be waived off along with royalties to the airports for using the infrastructure

- Bring ATF under the ambit of GST as for any airline in India, the cost of Aviation Turbine Fuel (ATF) forms about 40 per cent of the total operational cost

- As airlines experience a drastic decline in demand due to the coronavirus crisis, airport slot requirements should be temporarily waived. The rules currently governing slot allocation outline that airlines must operate 80 per cent, at the very least, of their allocated slots under normal circumstances, with failure to comply meaning that the airline loses its right to the slot during the next equivalent season. The coronavirus outbreak has drastically impacted the aviation industry and air traffic, with airlines experiencing severe declines in demand. Given the situation, the collective view of the airline industry is that the application of the 80 per cent rule during the upcoming season should be waived off

- Contingency fund need to be created by the government or some bailout package should be announced to financially support the aviation sector. Govt. has to intervene as this is a regulated sector

- Refer communication from Ministry of Finance dated 19th Feb, 2020, the current situation should be declared as a Force Majeure by the Aviation Ministry

- Moratorium or deferment of banks loan instalments due in next 6-month period

- GST payments to be made on realization instead of on accrual basis. This will help in cash flow management.

- Deferment of direct taxes for a period of 90 days.

- Instructing AAI not to charge Operations, Management and Development Agreement (OMDA) related royalties on the airports for a period of 6 months

- Many governments have announced financial “solidarity funds” to aide ailing sectors / companies to avoid mass scale layoffs the same should be done by the Government of India

Impact of COVID-19 on Shipping Sector

The shutdown of industries in China is negative for the Indian Exim cargo movement as India has significant trade linkages with China by way of import and export of raw materials and finished goods. Many industries like chemicals, dyes and pigments, pharmaceuticals, textiles, electronics, auto etc. could witness short-term supply disruptions due to a production shutdown in China. In turn, the reduced economic activity could result in a slowdown in bulk consumption and indirectly also affect bulk imports like coal, crude and other commodities. Further, with the movement of containers being affected by the cancellation of calls, re-routing cargoes and reducing calls there could be a disruption in the container cargo movement at Indian ports.

The coronavirus is threatening to disrupt this trade however timely safety measures and preventive actions by various ports and shipping organisations are expected to limit the impact of the outbreak

Challenges:

- Sailings are getting cancelled due to Covid-19 For example: 6-7 services are getting called at JNPT in comparison to 25-30 sailings in a month

- Shortage of empty containers especially from Dubai and Singapore with overall shipment volumes dropping to approx. 6-7 per cent

- Trade has collapsed, freight rates have dropped drastically and the ship owners are cash crunched

- In terms of Baltic Index Shipping rates have dropped from USD 1530 to almost USD 612

- Average freight earnings have dropped from USD 22600 per day to USD 2800 per day

Recommendations

- RBI should take out guidelines for non-payment of interest and principal for next 6 month. Also, if the payments do not happen for next six month the ship owners should not be declared NPA

- The crew on the ships are not allowed to sign off despite completing their tenure due to various restrictions at the ports. Like airline crew the shipping crew should be allowed to move after finishing their tenure

- The day to day operations have increased manifold for the Port Terminal Operators. They have to regularly follow up with Customs, health officers and immigration. These procedure approvals should be given online and should be expedited

Impact of COVID-19 on Solar Energy Sector

Indian solar industry sources around 80 per cent of its solar modules from China, making India’s expansive clean energy goals heavily dependent on one country. The remaining 15 per cent is imported from countries like Malaysia, Vietnam, Taiwan and South Korea.

But the spread of Covid-19 in China, where the virus originated, has caused factories to shut and brought cargo shipments to a halt. Additional impact also came due to Chinese New Year at the same time. India’s huge dependence on China has started impacting the solar sector in the following ways:

Challenges:

1. Most of the companies have got their last shipments in end January. Companies had kept a buffer for February due to New Year celebrations. However, factories have not started their operation in full capacity and are functioning at 30-40% PLF, therefore the production is not being able to keep up with the demand

2. Even with the existing supplies available, logistics is a problem. Shipping companies are not being able to ship the supplies to India and also restrictions at the Indian ports are further delaying the supplies

3. There is a demand glut in China. Even with China reducing their internal consumption by half, the supplies will not be able to meet the global demand unless factories start operating at 100% in the next 2 months. The earliest that Indian companies are expecting deliveries are mid-April (most optimistic) to mid-May

4. This delay in module supplies will impact the on-time completion of the solar IPPs in India. Govt. has a penalty for not completing projects on time, which will have to be paid by the power producers

5. The market predicts that the costs of solar modules will rise given the mismatch of demand and supply from China and the other module manufacturing countries will now be selling their modules at a premium. Around 12GW of solar projects are expected to be completed by the year end in India, of which around 10GW supply is dependent on China.

6. The rise in cost will also impact the tariffs of the projects bid out or future auctions, leading to an increase in solar power tariffs

7. The financial institutions are not willing to fund RE projects and many banks have cancelled/ stalled all funding. Also, since travel has been curtailed, the financing companies are not being able to travel to the project site for necessary clearances which is further delaying the financial approvals

8. Most companies have insurances for business interruption, which does not cover COVID19. Now the companies will have to secure fresh insurances to cover business interruption rising from COVID19, which will increase their overall operational costs

9. The other stakeholder industry like transmission etc. is also dependent on supplies from China which is also impacted, therefore the evacuation infrastructure are not getting completed on time, thereby impacting project completion

Recommendations:

- IPPs are looking at force majeure but this would depend on the PPAs signed and will differ for companies. Therefore, it is requested that blanket extension of about 3-4 months is given for completion of projects which are scheduled to be completed in the next 2 months. After this period the situation can be assessed, and a call maybe taken

- Since, working capital also gets impacted due to delayed in project completion, payment schedule should be relaxed, for a specific timeline and companies should not be declared NPAs. Also, payments from DISCOMs should become timely to address the working capital issue

- At present, basic customs duty (BCD) is at 20 per cent, however with safeguard duty at 15 per cent, the BCD is at 0. With safeguard set to go by end July, there is a need for clarity whether BCD will become effective post that, however request that BCD should be kept at 0

- This is the right opportunity for Govt. to look at promoting MII for solar manufacturing. Existing domestic manufacturers for solar, need to ramp up their production (current production not as per the factory capacity) and the GoI should look at subsidising the delta (about 3 to 5 cents) till this crisis tides over. This will help in running the Indian capacity at a higher percentage and also not slow the completion